Industrial storage is a high-margin market for semiconductor storage. Industrial application scenarios have higher requirements for memory performance stability, requiring memory manufacturers to have more advanced technical strength as support. With the development of autonomous driving and Internet of Vehicles, as well as the deepening of artificial intelligence applications and the increase of complex sensor arrays. The automotive industry's demand for memory is increasing day by day, and it will also become an important growth factor for the storage industry in the future. According to forecasts, the global automotive storage market will increase from US$2.2 billion in 2016 to US$8.3 billion in 2025, with a CAGR of 15.90%, and the proportion of automotive semiconductors will increase from 8% in 2019 to 12%.

Source: Sohu Automotive Research Laboratory

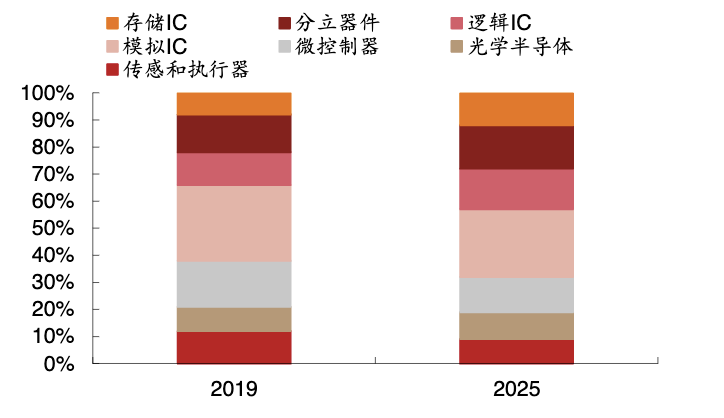

Automotive memory chip industry overview

Automotive chips can be divided into five major categories from the application stage: main control chips, memory chips, power chips, analog chips, sensor chips, etc. Among them, memory chips are mainly used for data storage functions, including memory DRAM (DDR, LPDDR4(x), etc.); flash memory FLASH (NAND FLASH, NOR FLASH); EEPROM, etc.

Specifically, DRAM and SRAM are most widely used in automotive scenarios, such as in-car entertainment systems, digital instrument panels, ADAS, high-definition map applications, driving recorders, etc. NAND is used in conjunction with DRAM and has similar application scenarios; NOR is mainly used in vehicle entertainment systems, ADAS, etc.

Smart cars have high requirements for instantaneous calculations. The vehicles need to process a large amount of data captured by sensors in real time, which puts forward higher requirements for bandwidth and space requirements. Compared with consumer-grade equipment, automotive-grade memory has higher requirements in terms of failure rate, reliability, and environmental adaptability. According to estimates, production costs are about 20% higher than consumer levels.

According to SemicoResearch data, for autonomous driving L1 and L2 levels, there is not much difference in the demand for storage capacity, which is generally configured with 8GB DRAM and 8GB NAND. High-precision maps, data, and algorithms for L3 and above autonomous driving require large-capacity storage to support: an L3 autonomous vehicle will require 16GB DRAM and 256GB NAND; an L5 fully autonomous vehicle is estimated to require 74GB DRAM and 1TB NAND. According to Micron Technology and China Flash Memory, L2/L3 autonomous vehicles require memory bandwidth of about 100GB/s, and the average capacity requirements for DRAM and NANDFLASH are about 8GB and 25GB.

Automotive memory chip market landscape

- DRAM

From the perspective of market structure, American and Korean companies are the majority, and domestic companies have also developed in recent years. As the absolute leader, Micron Technology has a market share of 45%. It conducted LPDDR5 sampling tests in 2021, leading the industry. Beijing Ingenics entered the field of automotive memory chips after acquiring Beijing Sicheng, and has reached close cooperation with downstream car companies such as Bosch Automotive and Continental.

Global automotive DRAM storage market share

- NAND Flash

The new four modernizations of electric vehicles drive NAND storage to evolve towards large capacity and high reliability, and demand capacity and value are increasing simultaneously. According to Western Digital forecasts, the NAND capacity required for bicycles will increase from 1TB to 2TB in 2022 and 2025. With the integration of the five major domains, the demand for NAND will reach 2TB+ in 2025.

Source: Car2Cloud data-driven smart driving future network

In terms of market structure, competition among China, the United States, Japan and South Korea is fierce, and infotainment and ADAS systems have driven the entire automotive industry's demand for large-capacity, high-performance NAND. Samsung's 256GB BGA SSD controller and firmware were independently developed by Samsung and have completed customer evaluation and are now in mass production, capable of achieving sequential read speeds of 2,100 MB/s and sequential write speeds of 300MB/s, respectively. Seven times and two times that of current eMMC. Western Digital, the domestic leader, has implemented the application of UFS memory in navigation maps, IVI systems, remote communications, ADAS and data logs.

- NOR FLASH: Demand for various vehicle systems is increasing, and Chinese companies occupy 70% of the market

There are currently the following structural growth opportunities in the automotive storage industry: on the one hand, the increase in system complexity has put forward higher demand for off-chip storage; on the other hand, more and more application scenarios are based on high-performance processing units, driving MCUs and GPUs. , MPU, SoC have storage requirements for programs and parameters, and FPGA has storage requirements for structured data. From the perspective of application scenarios, the upgrade of automotive ADAS systems, instrument systems, cruise systems and SOTA all require reliable NOR Flash storage.

Compared with DRAM and NAND Flash, NOR Flash is smaller. From the perspective of competition, China’s Macronix, Winbond and GigaDevice occupy the vast majority of the market share. In 2016 and 2017, Micron Technology, Sep. Lars has successively announced that it will withdraw from part of the NORFlash market competition and gradually faded out. The market share of NORFlash chips is gradually controlled by Macronix of Taiwan, Winbond and GigaDevice of China.