From a global perspective, competition in the semiconductor industry is still very fierce. At the same time, in order to seek greater development, cross-border cooperation between countries and regions continues to occur. In this issue, China exportsemi net Network will continue to interpret the second half of the " 2024 Global and Taiwan Semiconductor Industry Outlook " report for you. The main contents include: the aspects of competition and cooperation between the global and Taiwan semiconductor industries; and the forecast of the development direction of the global and Taiwan semiconductor industries.

- Aspects of competition and cooperation between the global and Taiwanese semiconductor industries

Leading major manufacturers to lead the process competition situation, mass production yield rate is key

The demand for efficient computing chips has driven the development of advanced process technology. TSMC, Intel, and Samsung, the three major semiconductor manufacturers, have invested heavily in trying to seize the opportunity of the latest process technology. The current process technology node has been advanced to 3nm mass production, and 2nm is expected to be launched from the end of 2024 to 2025. Subsequent more advanced process technology still needs to be developed.

Figure 1: Higher computing power requires more advanced process technology

R&D institutions and equipment manufacturers promote the development of advanced process technology

ASML plans to continue to improve its EUV equipment and will be able to produce component line widths below 1.1nm to meet the needs of more advanced process technology development; IMEC is promoting advanced process technology structures and process research and development directions below 2nm, which will be followed by wafer foundries. Continue to invest in relevant mass production technologies.

Figure 2: R&D institutions and equipment vendors promote the development of advanced process technology

HBM introduction to accelerate cross-industry integration and advanced packaging needs

HBM is a multi-layer stacked DRAM chip that achieves high-bandwidth data transmission performance through silicon through-holes and interconnects. HBM relies on high-level cooperation between major memory manufacturers, chip design, wafer manufacturing and advanced packaging companies to integrate.

Figure 3: HBM introduction to accelerate cross-industry integration and advanced packaging requirements

Supply chain restructuring and semiconductor autonomy drive cross-border competition

Affected by factors such as the Sino-US confrontation, the recovery of the post-epidemic supply chain and China plus one , a situation of multinational/cross-border cooperation and mutual competition has gradually taken shape.

Figure 4: Supply chain restructuring and semiconductor autonomy drive cross-border competition.

Semiconductors have become the main battlefield in the confrontation between China and the United States, and are also the focus of policies of various countries

In addition to the United States wooing allies to control mainland China, Taiwan, the United States, Japan, South Korea and mainland China have continued to invest in the semiconductor industry and are striving for opportunities in the development of the semiconductor industry. All parties cooperate with each other and compete with each other in a tense situation.

Figure 5: Semiconductors have become the main battlefield in the confrontation between China and the United States, and are also the focus of policies of various countries.

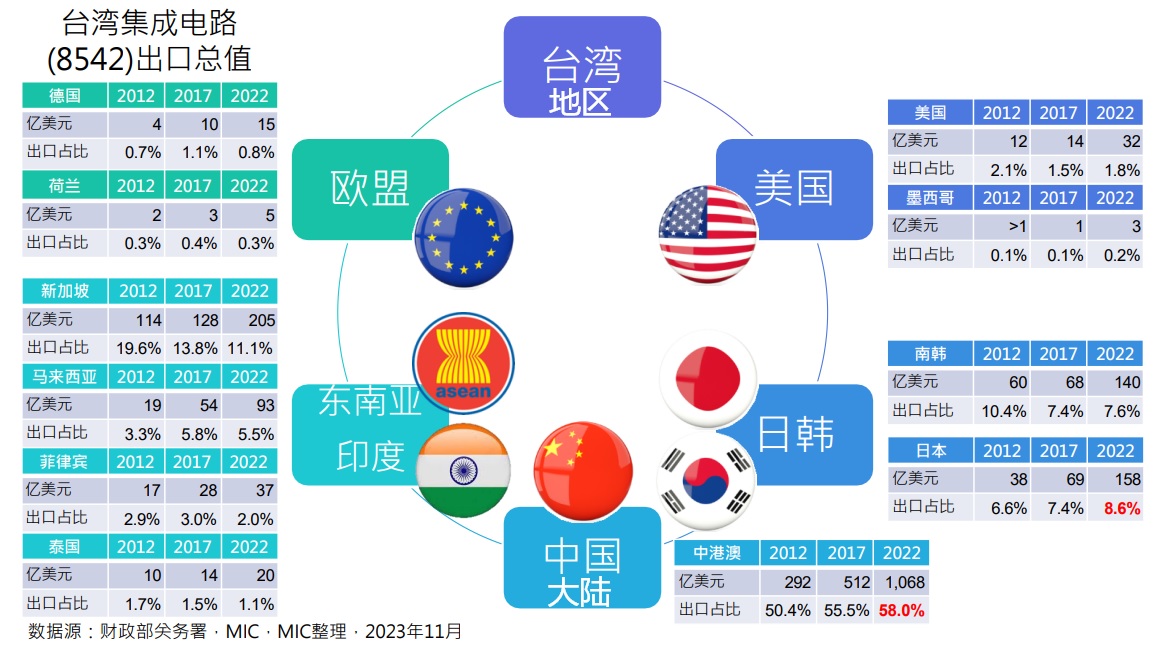

Cross-border cooperation remains the main theme, and Southeast Asia has become the new focus of deployment

Although the Netherlands also cooperates with US export controls, cross-border/cross-border cooperation still dominates, especially investment in Southeast Asia and India is the most eye-catching. European and American manufacturers have invested in Malaysia, Singapore, Vietnam, India, the Philippines and other places to build wafer factories, testing plants, packaging plants, etc.

Figure 6: Cross-border cooperation remains the main theme, and Southeast Asia has become the new focus of deployment

- Forecast of the development direction of the global and Taiwan semiconductor industry

Global semiconductor market development forecast

In 2023, external factors will impact enterprises and the consumer market, leading to a weakening of global purchasing power. Coupled with demand and inventory adjustments, the size of the global semiconductor market will plummet. It is expected that mainstream demand will recover in 2024 and emerging applications will explode. The market size will return to the level of 2022 and will continue to grow.

Figure 7: Global semiconductor market size from 2017 to 2026

Semiconductor industry development forecast in Taiwan

Data shows that Taiwan's semiconductor industry inventory fell to the bottom in 2023 and will resume growth in 2024, but the scale may not reach the level of 2022. Wafer foundry is still the main driving force for the growth of Taiwan's semiconductor industry. The memory market is expected to be driven by price recovery, and IC design still needs to make breakthroughs.

Figure 8: Taiwan ’s semiconductor industry output value from 2017 to 2024

Forecast of IC design industry development in Taiwan

Terminal operators' advance purchase of goods will affect peak season performance in the second half of the year, and it will still be difficult for output value to return to its peak performance in 2021. The AI craze will continue, and IC design companies are investing in diversified applications, but ROI still depends on mid- to long-term market cultivation.

Figure 9: Changes in output value & growth rate of IC design industry in Taiwan from 1Q22 to 4Q23

Forecast of IC manufacturing industry development in Taiwan

In addition to advanced manufacturing, operations in the second half of 2023 will still face sluggish demand, and capacity utilization and prices will be difficult to maintain. Major international memory manufacturers continue to reduce production, and it is expected that memory prices will stabilize in the short term and supply and demand will return to stability.

Figure 10: Changes in output value & growth rate of IC manufacturing industry in Taiwan from 1Q22 to 4Q23

Forecast for the development of IC packaging and testing industry in Taiwan

The peak season benefits in the second half of 2023 are expected to help the growth of the IC packaging and testing industry in Taiwan. Only by continuing to observe the dynamic recovery of the consumer market; HPC and AI emerging application trends continue to drive up the demand for advanced packaging, but in the short term, professional packaging and testing operators of limited help.

Figure 11: Changes in output value & growth rate of packaging and testing industry in Taiwan IC region from 1Q22 to 4Q23

Summary: Respond to global changes in the short term, prepare in the medium term and hope for long-term breakthroughs

compete:

Leading major manufacturers in deploying advanced nano-processes, hoping to attract high-end customers with efficiency and yield, but development and production costs will become key challenges for future production;

The global craze for electric vehicles, AI applications and intelligent networking continues unabated, stimulating the deployment of emerging chip companies and intensifying competition with existing IDM manufacturers in various countries and regions;

The confrontation between China and the United States is becoming long-term. The industries of the United States, Japan and Europe are facing competition in emerging fields. Southeast Asia and India are expected to rise. The semiconductor supply chain may become more complex.

cooperate:

Advanced multi-chip packaging enhances performance and cost flexibility, promoting cross-domain cooperation among memory, processor and related semiconductor manufacturing companies;

Autonomous driving technology and AI-based industries will lead cross-domain cooperation among chip, information and vertical industries, which is expected to promote the rise of emerging applications and create global business opportunities;

In order to maintain global economic stability, national security and scientific and technological development, friendly allies will strengthen semiconductor and scientific and technological exchanges and cooperation.

1. The "China plus one" strategy was originally proposed by Japan at the beginning of this century, which is to transfer part of the industrial chain to a third country. The Sino-US trade war and the COVID-19 epidemic have impacted global industries and accelerated companies' implementation of the "China Plus One" strategy.

Outlook for Taiwan’s Semiconductor Industry in 2024 (Part 1)

Outlook for Taiwan’s Semiconductor Industry in 2024 (Part 2)