In the context of the exponential growth of data storage demand, the two major requirements of "performance" and "energy efficiency" are jointly driving the rapid development of new storage technologies. For example, in the 70s of the 20th century, the demand for storage was only high read and write speeds, and the functionality and functionality of the PC era were designed for code storage, which required a small size. The era of intelligent terminals requires high-speed, high-capacity, and low-cost storage for data storage. In today's era of high-performance computing, the requirements for storage have changed to improve the energy consumption ratio and energy efficiency ratio, and new storage technologies are about to explode.

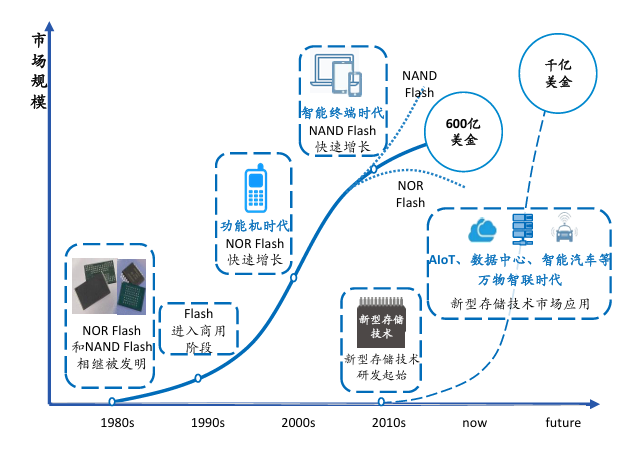

Emerging use cases are driving growth in the new storage market

According to Winsoul Capital, emerging applications such as AI and smart cars have put forward higher requirements for data storage in terms of speed, power consumption, capacity, and reliability, and the new storage technology aims to integrate the switching speed of SRAM and the high-density characteristics of DRAM, and has the non-volatile characteristics of Flash, with a market space of 100 billion yuan. According to Winsoul Capital, different memory types have different technical routes. For example, PCRAM has low latency and balanced read and write time. Long lifespan, writable ability far exceeds flash memory; Low power consumption, no mechanical rotation device; High density, some PCMs are non-transistor designed; It has good radiation resistance and can meet the needs of national defense and aerospace. MRAM is non-volatile, and the magnetism of ferromagnets does not disappear due to power failure; With fast write speed and low power consumption, it can realize instant power on and off and extend the battery life of the portable computer; It has a high degree of integration with logic chips, and has the potential to construct large-scale memory arrays on logic circuits. However, there is interference between memory cells, and the overlap of magnetic fields between adjacent cells will become more serious at high density. RRAM has a high speed, and the erase speed is determined by the pulse width of the trigger resistor transition, which is generally less than 100ns; High durability, reversible and non-damage mode for reading and writing; Multi-bit storage capability for increased storage density. FRAM has a fast-writing speed, which is more than 1000 times that of EEPROM and Flash; Low power consumption, the power consumption when writing is greatly reduced, which is 1/1000~1/100000 of EEPROM and Flash, and has the characteristics of long life and high read and write times. Each of these four technologies has its own unique advantages and challenges, and is suitable for different application scenarios and market needs. With the development of technology and the change of market demand, these new storage technologies are expected to play a more important role in the future storage market.

Figure: Emerging application scenarios are driving the growth of the new storage market

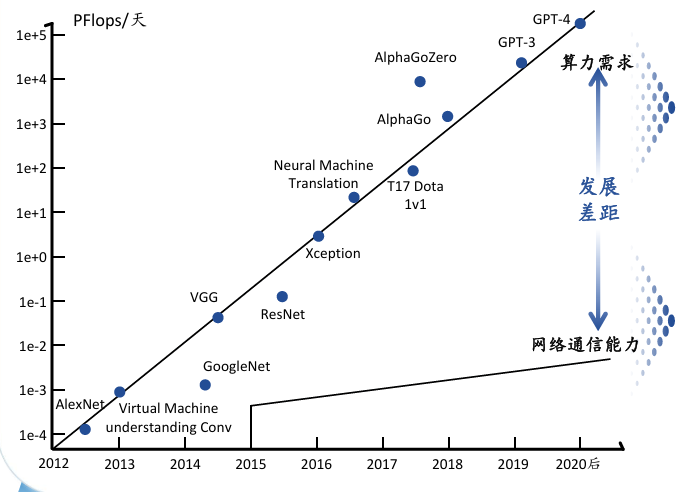

There is an urgent need for high-performance chips to improve the computing efficiency of AI infrastructure

At present, the distributed AI cluster system has changed from a computing constraint to a network communication constraint, which restricts the improvement of the overall computing efficiency of the infrastructure. According to Winsoul Capital, there is currently a mismatch between supply and demand between the capacity side and the computing power side. Due to the geometric growth of the demand for high computing power driven by large AI models, the demand for computing power for large model training doubles about every three months. IDC predicts that the compound annual growth rate of China's intelligent computing power will reach 52.3% from 2021 to 2026. In order to meet the computing power demand for model training in the AI era, the computing power of AI-accelerated hardware GPUs continues to grow, and GPU manufacturers accelerate their layout. However, the capacity side lacks a large-scale, high-performance, and low-latency network interconnection foundation. In the past five years, GPU computing power has increased by nearly 90 times, while network bandwidth has increased by only 10 times. The efficiency of cluster training decreases instead of increasing.

Figure: Due to the limitation of network communication capabilities, the computing efficiency of distributed AI clusters cannot increase linearly with the scale of computing power

The AI market is expected to be close to $1 trillion by 2027, with the AI hardware and services market likely to grow at an annual rate of 40% to 55%. As the scale of AI models expands, such as OpenAI's GPT model parameters from 170 million to 1 trillion, the demand for computing power has increased dramatically, and the development of high-performance chips is critical to improving the computing efficiency of AI infrastructure, which jointly promote the advancement and widespread application of AI technology by providing more computing power, optimizing energy consumption, supporting larger-scale model training and inference, and integrating advanced cooling technologies.

Related:

Outlook and Analysis of China Semiconductor Industry 2024 (1)

Outlook and Analysis of China Semiconductor Industry 2024 (2)

Outlook and Analysis of China Semiconductor Industry 2024 (3)

Outlook and Analysis of China Semiconductor Industry 2024 (4)