With the development of technology, various sensors are widely used in different fields and devices to acquire and process data. These sensors can be temperature sensors, humidity sensors, pressure sensors, light sensors, sound sensors, motion sensors, etc., they can detect various physical quantities in the environment and convert them into electrical signals, which can be used for data recording, monitoring, automatic control and other purposes. This market research report will analyze the road to multi-sensor integration based on the "Multi-sensor Era, the Road to Convergence is Opening - Perception of a Series of Reports on the Automotive Electronics Industry" released by Minsheng Securities.

Under the trend of decoupling software and hardware, the status of intelligent driving components has been improved

The improvement of intelligent driving components is mainly due to the fact that the automotive industry is undergoing a transition from traditional mechanical drive to software drive, and the transformation of electronic and electrical architecture makes automotive hardware tend to be centralized, and software differentiation has become a key factor in building automotive value. With the development of smart cars, software and service capabilities will become the most important competitiveness in the automotive industry.

In 2023, China will replace Japan as the world's largest auto exporter for the first time, breaking Japan's record of being the No. 1 auto exporter for seven consecutive years. According to data from the China Association of Automobile Manufacturers and the Japan Automobile Association, Japan's automobile exports in 2023 will be 4.42 million units, up 16% year-on-year, while China's automobile exports will be 4.91 million units in the same period, up 58% year-on-year.

The China Association of Automobile Manufacturers predicts that China's total car sales will exceed 31 million units in 2024, a year-on-year increase of more than 3%. Among them, the sales of passenger cars were 26.8 million, a year-on-year increase of 3%; Commercial vehicle sales were 4.2 million units, up 4% year-on-year. Among them, exports will continue to grow to 5.5 million units.

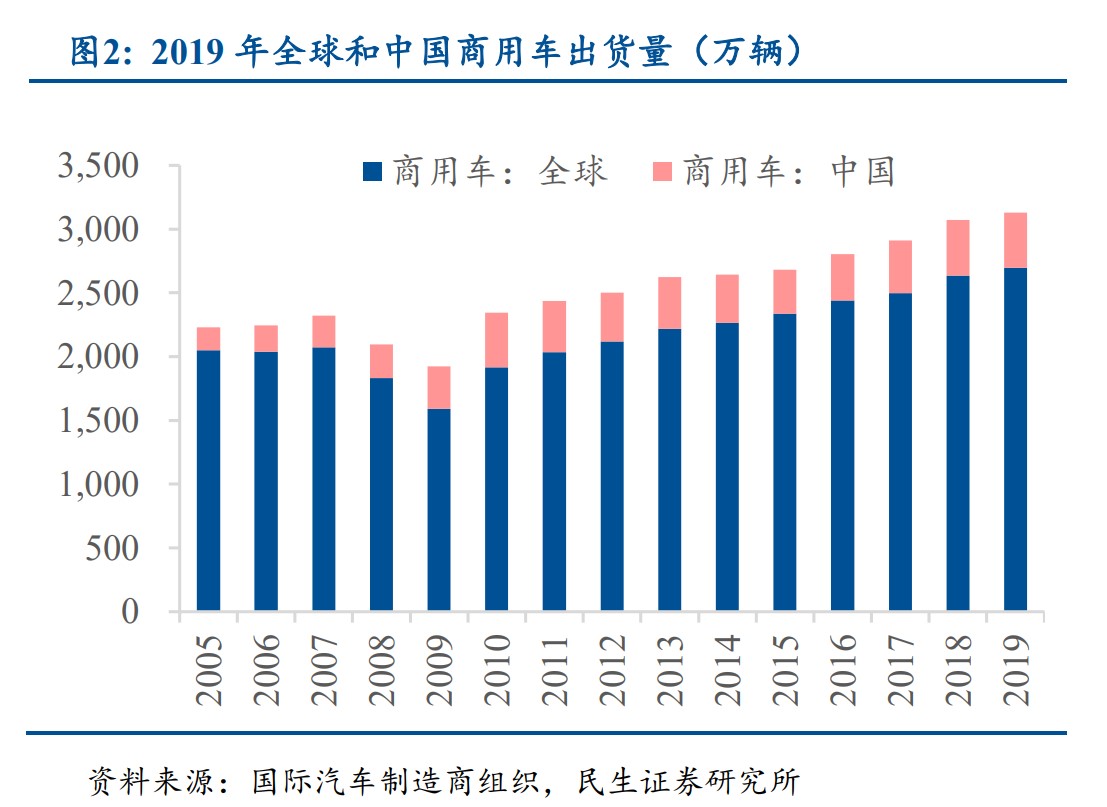

Figure: Global and China passenger car shipments in 2019 (10,000 units)

Focusing on the main line of automotive intelligence, the technical architecture can be divided into perception-decision-execution layer. According to the Ministry of Industry and Information Technology's "Classification of Automobile Driving Automation", autonomous driving can be divided into six levels: L0-L5. In terms of hardware configuration requirements, with the gradual degree of autonomous driving, multi-sensor fusion is required, which puts forward higher requirements for the performance and quantity of perception layer hardware such as cameras, ultrasonic radar, millimeter-wave radar, and lidar. The multi-sensor fusion perception system can complement each other, effectively cope with various complex conditions of light, weather, and road conditions in the real world, and form a redundant design in terms of safety.

The market size of intelligent driving components is expected to continue to grow. It is estimated that by 2030, the market size of the perception layer hardware driven by intelligent driving will reach 389.2 billion yuan, of which cameras, ultrasonic radars, millimeter-wave radars and lidars will reach 123.2 billion yuan, 33.2 billion yuan, 96 billion yuan and 136.7 billion yuan respectively. This shows that with the development of intelligent driving technology, the demand for perception layer hardware will continue to grow, promoting the development of related parts industry.

Figure: Sensor fusion process

Multi-sensor pre-fusion is a long-term goal, which is still in the early stage of intelligent driving development, and there is still a lot of room for hardware upgrades of the sensor itself. The development path of multi-sensor will tend to redundant re-fusion, and multi-sensor fusion will be gradually realized on the basis of the number of sensors installed and performance upgrades. LiDAR is still in the technology-driven stage, and it still needs to overcome the two mountains of automotive-grade mass production and cost reduction. On the other hand, the software part will also be iterated from the traditional controller algorithm to the deep learning vision algorithm to the enhanced learning decision-making algorithm, and the multi-sensor fusion algorithm will be iterated many times. Software and hardware walk on two legs, and eventually move towards integration.

The control point of traditional automotive technology lies in the efficiency of the whole vehicle, and the three core components with the highest value are the engine, gearbox and bottom

disks, other components and a wide variety of automotive electronic control systems are supplied by Tier 1 manufacturers. The cost of the three core parts of electric vehicles, such as battery, motor and electronic control, accounts for nearly 50%, and for smart cars, intelligent components, software, and intelligent cockpit will become the core of differentiated competition for automobile manufacturers. Industry insiders believe that in the future automotive industry chain, Tier0.5 integrators located in the middle of the traditional Tier1 industry chain will be born to fill the technology gap.

Follow China Exportsemi for more information, and the next article will analyze the industrial chain division of the perception layer.